Most people do not notice the tide moving in until their shoes are wet.

That is how real change arrives. Quietly at first, then all at once. A new tool here. A faster workflow there. A few jobs reshuffled. A few companies “disrupted.” We call it progress because the early benefits are obvious and the costs are delayed, distributed, and easy to dismiss.

But every now and then, progress stops being additive and starts becoming extractive. It stops improving the human condition and begins pressurizing it.

That is what I mean by catastrophic progress.

Adoption has moved past experimentation. The next step is operational dependence.

Figure 1. Businesses Using AI

Not because technology is “bad.” Technology is indifferent. The question is whether the incentives wrapped around it produce stability or fragility. Whether the gains widen opportunity or concentrate power. Whether the system adapts fast enough to prevent an efficiency breakthrough from becoming a social and economic shock.

And if you are a serious investor, you should care less about the headlines and more about the mechanics.

The acceleration trap

Here is the uncomfortable truth.

When capability compounds, society reacts linearly.

In the early phase, the story sounds familiar. “It will create new jobs.” “People will move up the value chain.” “Productivity gains lift everyone.” Sometimes that is true. Historically, it often has been.

But the current wave of automation is not just a better shovel. It is a substitute for judgment, coordination, persuasion, analysis, and execution. The work of knowledge workers. The work that sits inside law firms, accounting, marketing, finance, operations, customer support, and management layers. The work that props up household formation, consumer spending, and credit performance.

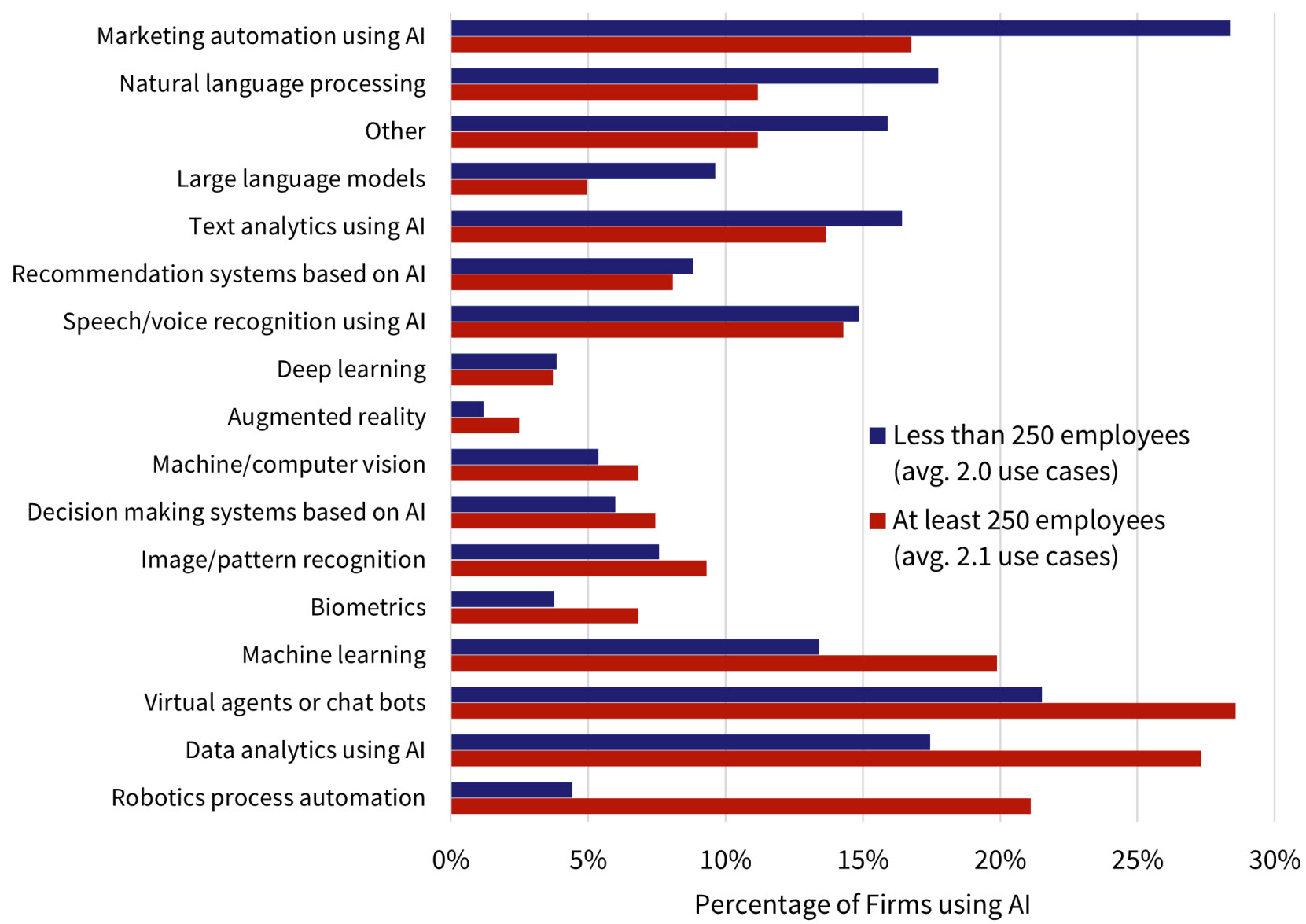

This is not a future roadmap. This is how firms are using AI right now.

Figure 2. Current AI Use Cases

And once you introduce software agents that can do tasks end to end, you do not need a one for one replacement. You need a fraction of the people to supervise a growing number of automated processes.

That is where progress can turn destructive. Not because companies hate people. Because competition hates slack.

If one firm cuts operating costs by 30 percent using automation, the next firm either follows or dies. If the first firm improves response times and quality while lowering price, the market punishes anyone who refuses to adapt. The moral debate loses to the quarterly report.

This is the loop that matters:

- Automation increases capability.

- Capability reduces labor needs.

- Reduced labor needs weaken household income growth.

- Weak income growth weakens consumer demand.

- Weak demand pressures margins.

- Margin pressure accelerates automation further.

That is not a theory. That is incentives doing what incentives do.

The danger is not a single job category being disrupted. The danger is a broad degradation of income reliability.

And income reliability is the foundation of every asset class you and I care about.

When income wobbles, credit follows

Credit is a confidence system. It works because the future is predictable enough to underwrite.

In a stable economy, lenders can model job stability, wage growth, and default patterns. In a stable economy, rent collections have an understandable relationship to local employment. In a stable economy, households can refinance, businesses can roll debt, and municipalities can project tax receipts.

When progress becomes catastrophic, what breaks first is not “the stock market.” What breaks first is underwriting assumptions.

If income becomes more volatile for large segments of the population, you can have “good borrowers” become fragile borrowers. Not because they are irresponsible. Because their cash flows become less dependable.

And once cash flows become less dependable, three things happen quickly:

1. Risk premiums rise. Investors demand more yield for uncertainty.

2. Duration becomes dangerous. Long dated assets get repriced because the future is less legible.

3. Liquidity becomes priceless. The ability to move becomes a competitive advantage.

This is why I pay close attention to anything that threatens the stability of household income. Because household income is the oxygen supply for consumer spending. And consumer spending is the oxygen

In investing, the greatest risk is not volatility. It is believing the future will resemble the recent past.

Real estate under catastrophic progress

Real estate is a cash flow business. Cash flows depend on tenants. Tenants depend on employment. Employment depends on the structure of the economy.

So the question is not, “Will technology change real estate?” It will.

The question is, “Which cash flows become more durable, and which become more fragile, when the economy gets reorganized?”

Here is how I think about it.

Segments that can prove resilient

Need-based retail and daily services in strong trade areas, where demand is tied to essentials and habitual consumption rather than discretionary optimism.

Logistics and last mile infrastructure that supports distribution, returns, and real-world fulfillment. Digital still hits the physical world somewhere.

Housing with real constraints where supply is structurally limited and demand is driven by necessity. You still have to live somewhere, even in a messy transition.

Well located infill real estate where replacement cost and scarcity create a buffer against repricing.

Resilience is not immunity. It is simply a higher probability that demand remains anchored.

Segments that can become vulnerable

Office tied to routine knowledge work that can be unbundled into automated workflows.

Experience driven discretionary concepts that rely on a broad middle class feeling confident.

Over-levered assets with thin credit quality where a small shock to income creates a big shock to collections.

Markets with concentrated exposure to industries that are automating fastest.

The underwriting shift is simple, but most investors will resist it because it forces humility.

You start treating tenant stability as a function of automation exposure. You start studying local industry concentration with more seriousness. You stop assuming a “normal” recession script. You stress test renewals, not just occupancy. You care less about the glossy pro forma and more about who is actually paying you.

And you get more conservative about leverage, because leverage is a bet on predictability.

What to do in the next 90 days

I am not interested in alarm. I am interested in readiness.

Here is a practical checklist sophisticated investors can execute without making heroic predictions.

1. Run a concentration audit

How much of your income is tied to employment sensitive demand?

How much is tied to a single metro, a single tenant, or a single industry?

Where are you implicitly short household stability?

2. Re-underwrite your leverage

If rates stay higher for longer, can every asset still service debt with a margin of safety?

If NOI dips 10 to 15 percent, what breaks?

What maturities are inside 24 months, and what is your refinancing plan if liquidity tightens?

3. Stress test tenant and customer exposure

Which tenants depend on payroll heavy cost structures?

Which tenants are intermediaries, selling “coordination” that software can replicate?

Which tenants have pricing power, or are they one bad quarter away from cutting locations?

4. Upgrade your liquidity posture

Liquidity is not a return drag in uncertain regimes. It is an option.

Build a reserve that lets you act when others cannot.

Do not confuse “fully invested” with “fully prepared.”

5. Tighten counterparty and sponsor diligence

In a transition, execution matters more than projections.

Back operators with discipline on expenses, leasing, and capital planning.

Avoid deals that only work if the world stays polite.

6. Be selective with enabling infrastructure

There will be real opportunity in the picks and shovels of the new era: power, data infrastructure,

specialized industrial, and critical logistics.

But do not treat it like a free lunch. Overcrowded trades still lose money.

Favor assets with durable demand drivers, not just narrative momentum.

7. Recommit to underwriting simplicity

Avoid complexity that depends on perfect outcomes.

Prefer clear cash flow, conservative assumptions, and a margin of safety.

If you cannot explain the risk in two sentences, you probably do not understand it.

The point

Catastrophic progress is what happens when human systems cannot absorb the speed of capability.

We are entering a period where efficiency can outpace society’s ability to distribute opportunity, protect stability, and preserve trust in the future. That is not a reason to panic. It is a reason to lead.

Capital has responsibilities. To your family, to your partners, and to your communities. The goal is not to predict every twist. The goal is to build portfolios that can take a punch, stay liquid, and keep optionality when the next era rewrites the rules.

Progress is coming either way.

The only question is whether you are positioned to benefit from it, or to be blindsided by it.